The U.S. housing market has experienced remarkable boom-bust cycles since the 1970s. Most recently, the pandemic boom substantially eroded the affordability outlook for homebuyers and investors looking to gain a foothold in the market. Inflation-adjusted house prices remain more robust than most analysts anticipated, with mortgage rates elevated. The path to reclaiming a balance—without a housing bust—appears difficult.

Source: Federal Reserve Bank of Dallas

Article by:Enrique Martínez García and Lauren Spits

However, a review of market-based and private forecasters’ expectations suggests that U.S. housing may be at an inflection point. U.S. income growth and, more broadly, the robust U.S. labor market are expected to alleviate the pandemic-era excesses that led to rapidly deteriorating affordability. This contrasts with a house-price correction in other global economies, such as Germany.

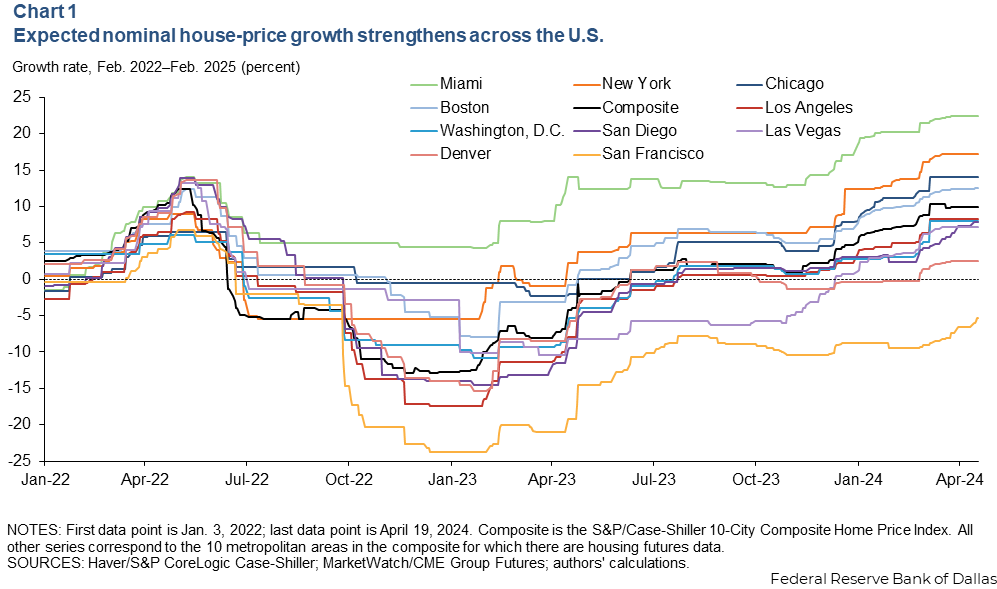

House prices firming up, but regional differences increasing

Futures contracts, and more specifically housing futures contracts, are financial instruments for investors to hedge price risks associated with housing portfolios. These housing futures provide insight into what market participants anticipate house prices will be at different time horizons. Although traded in mostly thin markets, futures tell us something about the evolution of financial investors’ views on housing that are broadly consistent with private forecasts.

Chart 1 illustrates how rising interest rates from March 2022 through July 2023 weakened market-based expectations of future nominal house-price appreciation only temporarily across major U.S. metros before bouncing back beginning in early 2023.

There has also been a widening in the variation in expected growth across metropolitan areas. Two outliers, Miami and San Francisco, stand out. Miami can still expect significant house-price growth, while San Francisco could be in for substantial declines, according to futures investors.

Overall, the futures predict robust nominal house-price growth rather than the severe correction feared by many—including the markets—early on. One possible reason for this is the surprising strength of the U.S. economy—notably since 2023—even in the face of significantly higher interest rates than in the past two decades. Some of the movement is attributable to tailwinds from improving supply chains and the recent migration surge into the U.S.

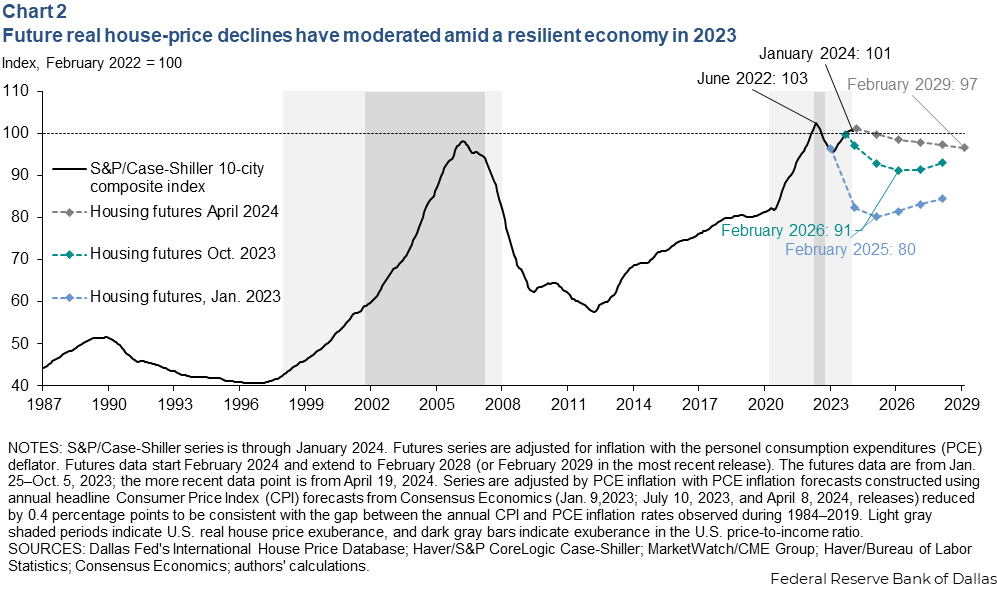

From a severe correction to a soft landing for U.S. housing

The pandemic housing boom is readily apparent after adjusting for inflation to make values more comparable across time (Chart 2). Projections inferred from housing futures data for the U.S., combined with survey data on inflation, show how market-based U.S. housing expectations have evolved.

In January 2023, market participants anticipated a severe house-price decline of around 20 percentage points from February 2022 to February 2025, after adjusting for inflation. Had this correction materialized, almost all the gains made in real house prices during the pandemic boom would have already disappeared.

Market expectations drastically shifted by October 2023 to a more modest and gradual correction of around 9 percentage points from February 2022 to February 2026 (adjusting for inflation). The drop is less than half the decline expected at the beginning of 2023 and would take longer to unfold.

The April 2024 futures indicate a lesser and still more gradual decline than indicated by the October 2023 data—3 percentage points from February 2022 to February 2029. Taken in context, the latest futures data point to house prices growing slightly below the rate of inflation over the next five years.

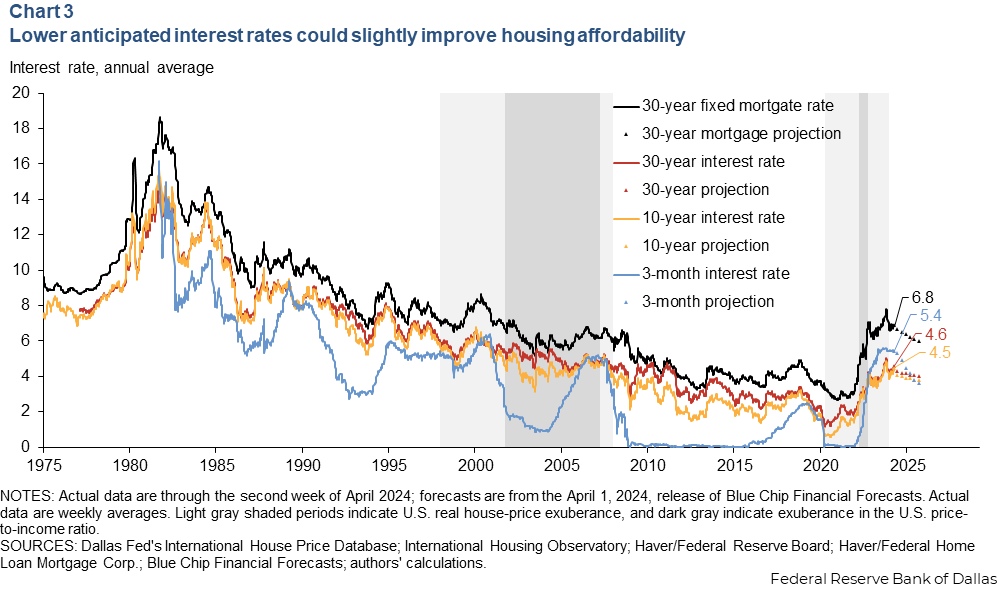

Affordability can improve without a house-price correction

With downward pressure on real house prices easing, how might the housing market regain its footing without a decline? Pandemic-era housing prices propelled historically high levels of unaffordability. Lower interest rates, though remaining above prepandemic levels, may provide some relief (Chart 3 ).

With interest rates forecast to decline only modestly over the next two years, they can only explain a small part of the path toward improved affordability.

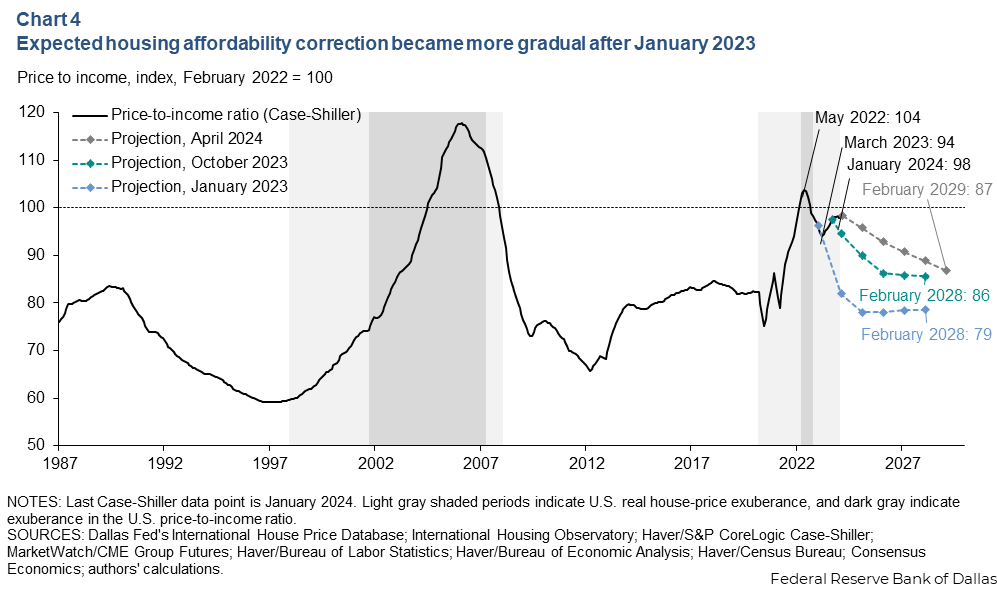

The personal disposable income component of the house price-to-income ratio is the other key dimension of a housing affordability correction. The projection of this ratio shifted expectations toward a more gradual affordability improvement between January 2023 and April 2024. Income growth rather than lower real house prices is projected to pace the improved outlook (Chart 4).

Chart 4 suggests that under the relatively benign scenario in April 2024, the price-to-income ratio should decline by about 13 percentage points by February 2029 relative to February 2022 levels. Such a drop would retrace approximately two-thirds of the pandemic-era increase.

Putting it all together, the affordability correction in the U.S. is not expected to arise from a house-price bust but rather from strong income growth in a scenario with moderate house-price appreciation that slightly trails inflation.

While slowly improving housing affordability can be less disruptive than a disorderly house-price bust, there remain associated risks. First, the more gradual correction tempers labor mobility as households face financial constraints that, in turn, limit relocation options in the event of future economic shocks.

Second, household formation can be delayed as a result, which can have demographic implications. Third, sellers may encounter increased time and cost risks because fewer people are buying homes.

Finally, prolonged unaffordability can increase the odds of a severe correction in a future house-price run-up, inducing a negative wealth effect on economic activity and a restraining of household consumption. Additionally, there is evidenceindicating that homes might still be overvalued, and thus, the market might be further away than initially thought from resolving the pandemic excesses. Such an extended horizon provides another source of risk and possible threat to financial stability.

Why were previous gloomy forecasts off base?

The shift from a pessimistic outlook of a sharp house-price correction to a more optimistic one in 2024 begs the question of why the previously bleak forecasts seem to have missed the mark.

Two likely factors contributed to a less difficult transition than was indicated in early 2023.

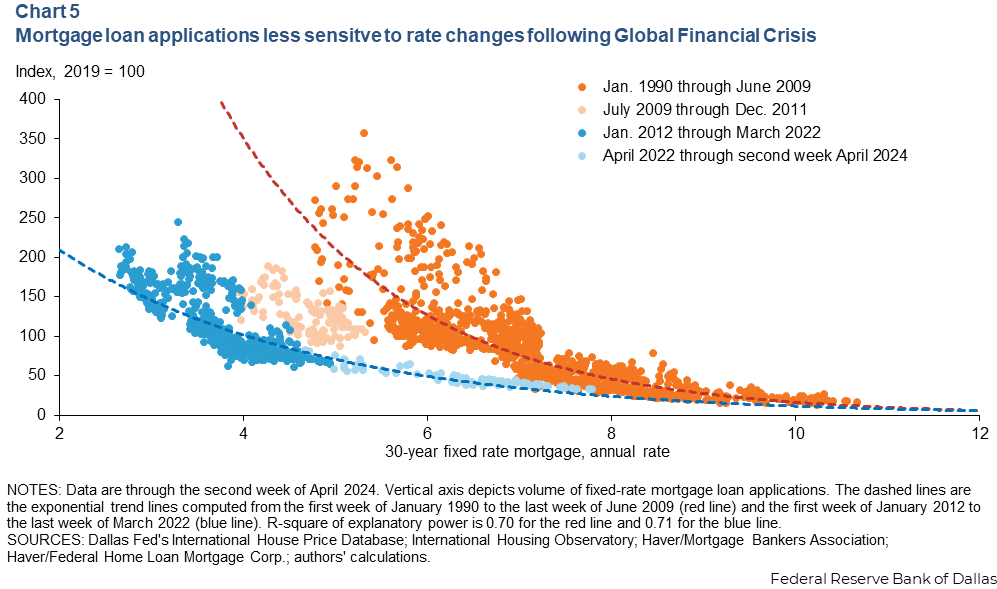

First, the banking industry has been resilient in the post-Global Financial Crisis (GFC) period and through the pandemic era. Regulatory changes required by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 as well as generally tighter lending standards among banks may have contributed to a downward shift in the relationship between interest rates and mortgage activity (Chart 5 ). Improved mortgage quality played a role, too.

Still, other factors likely included the differences in the composition of outstanding loans (rate, age, outstanding balance) and changes in market liquidity. Also, the GFC-era collapse of the private-label securitization channel (packages of mortgages assembled by nongovernment entities and sold to investors) and associated product offerings—which created refinance churn—altered the overall mortgage market. Furthermore, until 2018 the federal Home Affordable Refinance Program (HARP) allowed some homeowners to refinance at lower interest rates even though they owed more than their properties were worth.

The second key to the changed mortgage outlook was the unexpectedly resilient labor market. Federal Reserve Governor Christopher Waller observed in July 2022 that the labor market appeared to be headed for a soft landing. He suggested such an outcome was possible given that the job vacancy-to-unemployment rate was at an unprecedented high during the pandemic. It would be feasible, he said, to reduce the number of vacancies without a large, adverse impact on the unemployment rate. The robustness of the labor market in this context explains much of the forecasting misses on growth but also, we argue, regarding housing during 2023.

To the extent that the Waller hypothesis is correct, a soft landing for the economy, whereby the unemployment rate increases modestly but remains historically (and internationally) low, would arguably also continue to support the housing market while improving affordability through sustained income growth.

About the authors:

Enrique Martínez García is an assistant vice president in the Research Department at the Federal Reserve Bank of Dallas.

Lauren Spits is a former research analyst in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}